{kind=link}

Over the previous few months, there was a rise within the variety of financial institution accounts belonging to cryptocurrency professionals which were frozen or restricted within the UK, US and EU. They are saying you usually do not care about one thing till it occurs to you; effectively, it did this week. To my actual shock, it got here from one place I least anticipated.

Revolut has lengthy been thought-about essentially the most crypto-friendly financial institution within the UK, providing in-app purchases of crypto, and in 2023 it’s lastly including the flexibility to ship and obtain crypto, albeit with some restrictions. Nevertheless, latest occasions have forged doubt on the financial institution’s dedication to offering clients who use cryptocurrencies with a seamless expertise.

Regardless of the UK not being a part of the European Union beneath MiCA EU rules, the newly applied journey rule requires related info. Because of this customers are actually required to reveal and establish the homeowners of all non-hosted wallets which can be recipients of Revolut withdrawals.

Nevertheless, UK crypto corporations can use a risk-based strategy to find out when they need to accumulate details about non-hosted wallets. They merely want the flexibility to establish the place their clients are transacting with non-hosted wallets and assess the riskiness of these transactions.

How the UK’s most crypto-friendly financial institution froze my 0.23 ETH account

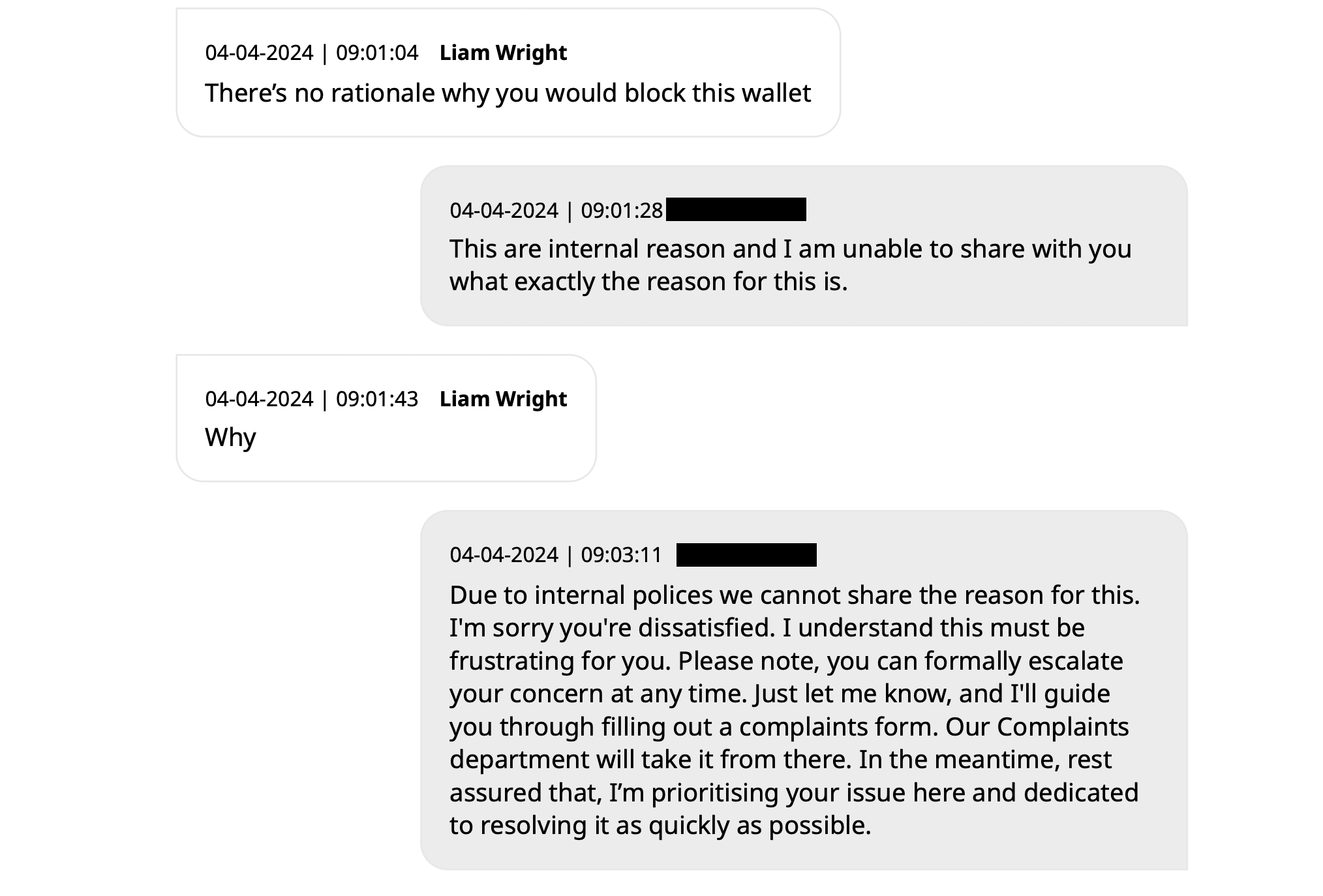

Two days in the past I purchased a measly 0.23 ETH (£550) by the Revolut app and tried to switch the funds to my private Ethereum pockets, which is linked to the well-known ENS area. To my shock, Revolut blocked the transaction and deducted the charges from the account. As well as, my whole checking account was frozen, together with the joint account with my spouse.

After a number of hours of frustration and confusion, the account was lastly unfrozen and the fees refunded after one other request. Nevertheless, the precise pockets tackle stays blocked, stopping me from sending funds to this account. This expertise left me questioning the true nature of Revolut’s supposed crypto-friendliness. Given the alternate options within the UK, Revolut stays the best choice for these unhappy with conventional banks, nevertheless it’s a low bar. I consider incidents like these have much less to do with Revolut being “anti-crypto” and extra to do with concern of regulatory retribution.

Nonetheless, a chat transcript between the Revolut help crew and myself reveals an absence of transparency relating to the explanations for account freezes and pockets tackle blocking. Help representatives have been unable to supply a transparent clarification, citing inside insurance policies that forestall them from disclosing particular causes for these actions.

The incident raises issues in regards to the autonomy and management Revolut customers have over their very own funds, particularly relating to digital asset transactions. Blocking a private pockets tackle and not using a passable clarification undermines confidence within the financial institution’s capacity to facilitate easy crypto transactions.

Because the UK navigates the post-Brexit monetary panorama, banks like Revolut should strike a steadiness between compliance and offering a user-friendly expertise for his or her clients. Strict enforcement and lack of transparency when coping with account and pockets points danger alienating cryptocurrency customers who depend on these providers. That is very true on condition that the corporate is making an attempt to open up a specialised crypto change providing.

Debanking cryptocurrency customers in the US

In the US, even cryptocurrency customers who’ve been longtime clients of conventional banks are going through account closures as a result of their involvement in digital property. John Paller, co-founder of ETH Denver, not too long ago shared his expertise on Twitter, revealing that Wells Fargo kicked him out of his checking account after 26 years of sponsorship and thousands and thousands paid in charges. Paller’s checking, financial savings, bank cards, private traces, nonprofit and enterprise accounts have been all closed with out clarification, regardless that he had not not too long ago used his private accounts for cryptocurrency purchases.

Caitlin Lengthy, founder and CEO of Custodia Financial institution, responded to Paller’s tweet and famous a big enhance in inquiries from crypto corporations urgently in search of to interchange financial institution accounts closed by their banks. She referred to as the development the subsequent wave of “Operation Choke Level 2.0,” suggesting a full-on witch hunt towards cryptocurrency-related companies.

Bob Summerwill, director of the Ethereum Basic Cooperative, echoed this sentiment and emphasised the necessity for banks like Custodia. He shared his personal expertise with PayPal closing the Ethereum Basic Cooperative account with out giving particular causes, solely stating that the choice is everlasting and can’t be reversed.

These incidents spotlight a rising concern within the crypto neighborhood: even those that have established relationships with conventional banks and have a historical past of compliance are vulnerable to dropping entry to banking providers. The dearth of transparency and sudden nature of those account closures raises questions in regards to the underlying motivations behind these actions and the potential influence on the expansion and adoption of cryptocurrencies in the US.

Optimistic friction actually simply means a horrible consumer expertise

I’ve additionally heard anecdotally from not less than 5 different people who work in cryptocurrencies and frequently transfer important quantities of FIAT forex by conventional banks which have frozen accounts. I am not advocating the Wild West; Widespread sense regulation is all I ask.

The UK’s strategy to regulation additionally contains what it sees as “optimistic friction”. This idea refers to a set of regulatory measures designed to impose sure obstacles or controls that decelerate the method of investing in digital property. These measures are supposed to counteract social and emotional pressures which will lead people to make rash or ill-informed funding selections. The Monetary Conduct Authority (FCA) launched these “optimistic frictions” as a part of its monetary help laws to enhance client safety within the crypto market.

Particular examples of “optimistic friction” embrace personalised danger warnings and a 24-hour cooling-off interval for first-time traders with the agency. These measures are designed to make sure that people are adequately knowledgeable in regards to the dangers related to crypto-investing and have enough time to rethink their funding selections with out the affect of rapid emotional or social pressures.

The fact is a sequence of questions designed to scare off new traders, adopted by an ugly warning banner on the high of each crypto app that by no means appears to go away even in the event you meet all the necessities.

I’m wondering when the federal government will introduce a fractional reserve banking take a look at for all conventional finance clients? We have to know in regards to the nuances of presidency regulation of cryptocurrencies, reminiscent of who oversees the FCA and whether or not a whitepaper is required. Suppose we have been to ask ten folks on the road what occurs once you put cash into their checking accounts. I’m wondering what number of would cross the take a look at?

How many individuals know that the minimal reserve necessities of US and UK banks are 0%? The earlier limits of 5-10% have been abolished in 2020, and now it’s as much as the financial institution to determine how a lot of its purchasers’ funds it should really maintain in money. Subsequently, it’s completely authorized for a financial institution to take a £1,000 deposit and lend the total quantity to a different get together.

In fact, conventional finance is regulated and the cash is ‘assured’ by authorities insurance coverage, so we do not have to fret. Let’s simply not look again to 2008 after we needed to depend on such instruments, lets? Lower than 10% of shoppers wanted to withdraw funds from Northern Rock earlier than the collapse occurred.

Banks do not have all of your cash; effectively run crypto exchanges and proprietary wallets sure, however do rules recommend we must be afraid of cryptocurrencies?

I believe it is the banks which can be scared.

I requested Revolut help and the X groups if the PR division want to touch upon my scenario previous to this op-ed, however the query was repeatedly ignored.